Table of Content

Plans should set out the contributions expected from development. This should include setting out the levels and types of affordable housing provision required. Subject to the transitional arrangements set out in paragraph 018, this should include policies for First Homes.

You must give them the same percentage discount that you got, based on the home’s market value at the time of sale. Evidence would typically be in the form of a detailed viability assessment prepared in line with Planning Practice Guidance on Viability in Decision Taking. For decision making, what constitutes a proportionate development will vary depending on local circumstances. Mandatory social housing relief can apply in respect of dwellings where the first and subsequent sales are for no more than 70% of their market value.

Plan- and Decision-Making

Homebuyer.com offers a nationwide forgivable mortgage through our instant mortgage application. Recipients must have an average credit rating, qualify for anFHA loan, and agree to use a 30-year fixed-rate mortgage, among other qualifications. Five years later, if the buyer still lives in the home and has made on-time payments as agreed, the lender will write off the smaller $15,000 mortgage. In late 2022, the Federal Housing Finance Agency discounted interest rates to make homes more affordable for first-time buyers.

One of the biggest challenges is keeping your savings in an accessible, relatively safe vehicle that still provides a return so that you’re keeping up with inflation. Consider the type of residence that will serve your needs, what you can afford, how much financing you can secure, and who will help you conduct your search. Ebony Howard is a certified public accountant and a QuickBooks ProAdvisor tax expert.

Get your credit report

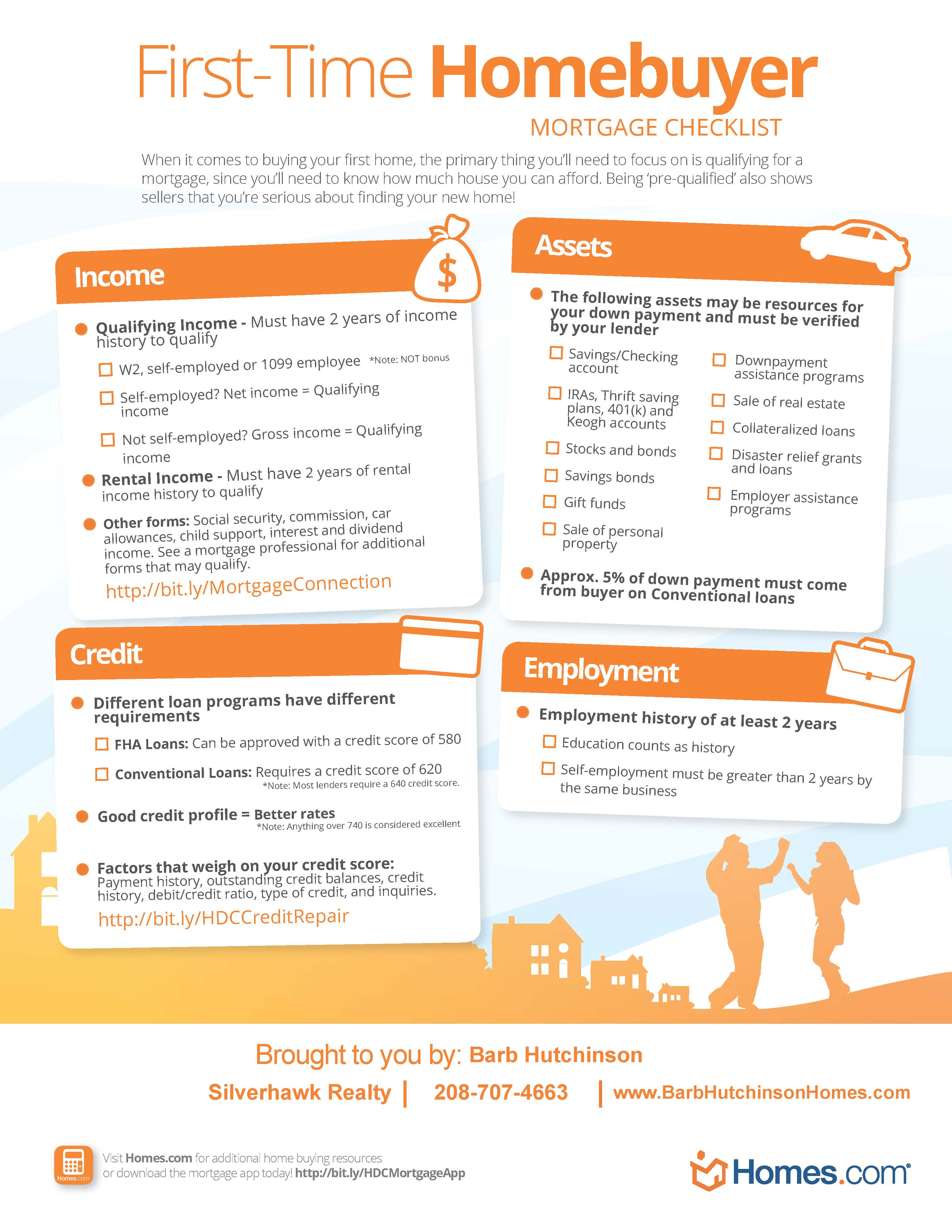

For example, if you bring $25,000 of your own money to a $250,000 home purchase, you have made a 10% down payment. The remaining amount — $225,000 — is covered by your mortgage loan. No one expects you to be an expert on the home-buying process, especially when you’re a first-time buyer. Typically, eligibility in these programs is based on income and, often, on the size of a property’s purchase price.

If you’re taking out a mortgage to buy your home, an appraisal will be required so that the lender is assured they aren’t loaning you more money than the home is worth. Even if you’re buying in cash, it’s probably a good idea to have an appraisal in order to ensure you’re not overpaying. The first step to buying a home is to learn what kind of ground you’re standing on from a lender’s perspective — and that means knowing your credit score. Your credit score affects the rate and amount of mortgage loan you can get, so knowing what your score is and correcting any problems will be important for you to get a good deal on a mortgage. $350,000 and less than $450,000 The eligible purchaser can choose to pay a concessional transfer duty rate under FHBA or, not pay duty and instead opt into paying an annual property tax under FHBC.

Can the price cap be changed?

They require lower down payments for eligible participants, and often sell at below market prices. You can take advantage of federal, state and local government programs when you buy a home. Federal programs are open to anyone who’s a citizen or legal resident of the U.S.

FHA loans allow buyers with credit scores as low as 580 with 3.5% down, and 500 with 10% down. However, low credit scores must not be the result of recent bad credit history. Conventional 97 mortgages offer no such discount but can be the most economical way to purchase a home with little money down (just 3%) — especially for buyers with extra-good credit.

What is a first-time home buyer?

With homeownership comes major unexpected expenses, such as replacing the roof or getting a new water heater. Start an emergency fund for your home so that you won't be caught off guard when these costs inevitably arise. It’s easy to be ambushed by higher or unexpected utilities and other costs if you are moving from a rental to a larger home. For example, you might request energy bills from the past 12 months to get an idea of average monthly costs.

To get a first-time home buyer grant, you’ll have to look for programs where you live. These grants are typically offered by state and local governments and nonprofits, so they vary by area. To qualify, you generally need to be a first-time home buyer with low-to-moderate income. You’ll also need to make sure the mortgage program you’re applying for allows you to use the funds toward your down payment and/or closing costs. First-time buyer programs include mortgage rate reductions, down payment and closing cost assistance programs, and federal and state tax credits for first-time buyers of homes. The term first-time homebuyer generally refers to an individual who purchases a principal residence for the very first time.

If you aren’t sure whether you qualify, the best thing to do is talk to a Home Loan Expert at Rocket Mortgage. They can take a look at your unique situation and point you in the right direction. Most government home buying assistance comes through state and local programs. You can view a complete list of state-specific buying resources on the HUD website. Ready Buyer™ program is only available to first-time buyers who want to live full-time in a house that they’re looking to purchase.

You can only sell the home to someone who is eligible to buy a First Home. Developers offer these homes to first-time buyers with 30% to 50% of the market value taken off the price. Applicants will be expected to provide evidence of this need in the form of a Local Housing Needs Assessment, local authority Housing Register, or other sufficiently rigorous local evidence. Policies for First Homes should reflect the requirement that a minimum of 25% of all affordable housing units secured through developer contributions should be First Homes.

One of the best places to search for such incentives is through local and state government websites. Text for the bill saysthat first-time homebuyers of a principal residence in the U.S. could claim a tax credit equal to 10% of the purchase price of the tax residence during that tax year. Depending on your tax-filing status, the bill limits the credit to $7,500 for married individuals filing separately. As a buyer, just keep in mind that mortgage pre-approval is different from mortgage pre-qualification.

No comments:

Post a Comment